The Global Automotive Intercooler Market is an essential segment of the automotive thermal management industry. Intercoolers, or charge air coolers, are heat exchangers used to cool the air compressed by turbochargers or superchargers before it enters the engine's combustion chamber. By increasing air density, intercoolers significantly improve engine efficiency, power output, and fuel economy while simultaneously reducing harmful emissions.

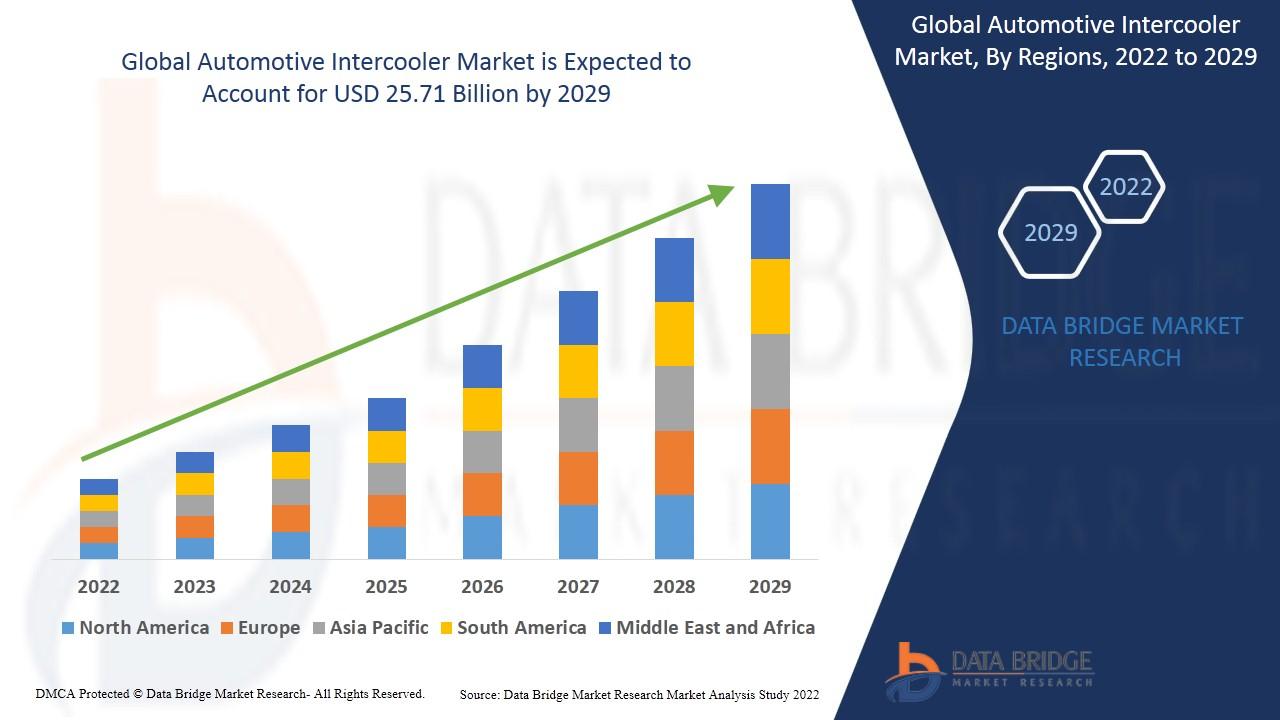

Data Bridge Market Research analyses that the automotive intercooler market would exhibit a CAGR of 6.94% for the forecast period and is expected to reach USD 25.71 billion by 2029.

Market Size and Growth Trajectory

As of late 2025, the global automotive intercooler market is valued at approximately USD 18.8 billion to USD 19.8 billion. The market is projected to reach approximately USD 24.1 billion to USD 25.7 billion by 2030, exhibiting a steady Compound Annual Growth Rate (CAGR) of roughly 5.0% to 5.4%.

While the rapid shift toward electric vehicles (EVs) poses a long-term challenge to traditional intercooler demand, the market remains robust due to the "downsizing" trend in internal combustion engines (ICE), where smaller engines rely on turbocharging—and thus intercoolers—to maintain high performance levels.

Core Market Drivers

Several structural and regulatory factors are currently shaping the intercooler landscape:

-

Engine Downsizing and Turbocharging: Automakers are increasingly replacing large, naturally aspirated engines with smaller, turbocharged versions. This allows for better fuel efficiency without sacrificing horsepower. Since a turbocharger is ineffective without an intercooler to manage heat, this trend is the primary driver of market volume.

-

Stringent Emission Regulations: Global mandates such as Euro 7 and CAFÉ (Corporate Average Fuel Economy) standards require manufacturers to optimize combustion. Cooling the intake air reduces the temperature of the combustion process, which significantly lowers the production of nitrogen oxides ($NO_x$), helping vehicles meet environmental compliance.

-

Rising Demand for High-Performance Vehicles: The growing consumer preference for SUVs and high-performance sports cars, which frequently utilize forced induction (turbo/supercharging), continues to sustain the demand for high-capacity, efficient intercoolers.

-

Hybrid Vehicle Integration: Many hybrid electric vehicles (HEVs) still utilize turbocharged ICEs as part of their powertrain. These systems require compact, highly efficient intercoolers to balance weight and thermal performance within complex engine bays.

https://www.databridgemarketresearch.com/reports/global-automotive-intercooler-market

Market Segmentation: Technology and Design

The market is diversified based on cooling methods and vehicle architecture:

By Type (Cooling Medium):

-

Air-to-Air Intercoolers (Dominant Segment): These hold the largest market share (approx. 62%) due to their simplicity, reliability, and cost-effectiveness. They use ambient air to cool the charge and are standard in most passenger and commercial vehicles.

-

Air-to-Water Intercoolers (Fastest Growing): These systems use engine coolant or a dedicated liquid circuit to remove heat. They are becoming more popular in high-performance and compact engine designs because they provide more consistent cooling and allow for more flexible engine bay packaging.

By Vehicle and Engine Type:

-

Passenger Cars: The largest vehicle segment, driven by the mass adoption of turbochargers in compact and mid-sized sedans.

-

Turbocharged Engines: Account for over 60% of the engine-type segment, as they have become the industry standard for modern ICE efficiency.

By Mounting Location:

-

Front-Mounted (FMIC): Preferred for maximum airflow and cooling efficiency.

-

Top-Mounted (TMIC) and Side-Mounted: Often used in specific vehicle architectures where space is limited or for specific aerodynamic goals.

Regional Market Insights

Conclusion

The Global Automotive Intercooler Market is at a strategic crossroads. In the short to medium term, the market is bolstered by the global transition to turbocharged, fuel-efficient ICE and hybrid powertrains. However, the long-term outlook is increasingly defined by the industry's pivot toward full electrification. To remain competitive, manufacturers are shifting their R&D focus toward advanced thermal management systems for hybrids and lightweight materials, such as aluminum and 3D-printed composites, to reduce vehicle weight. While the traditional intercooler may eventually face a decline in a post-ICE world, the expertise in high-efficiency heat exchange will remain a critical asset as vehicles move toward complex, multi-circuit cooling requirements for batteries and power electronics.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com