How Is Consumer Awareness Driving Health Food Trends in North America?

Causes |

2026-03-17 08:32:05

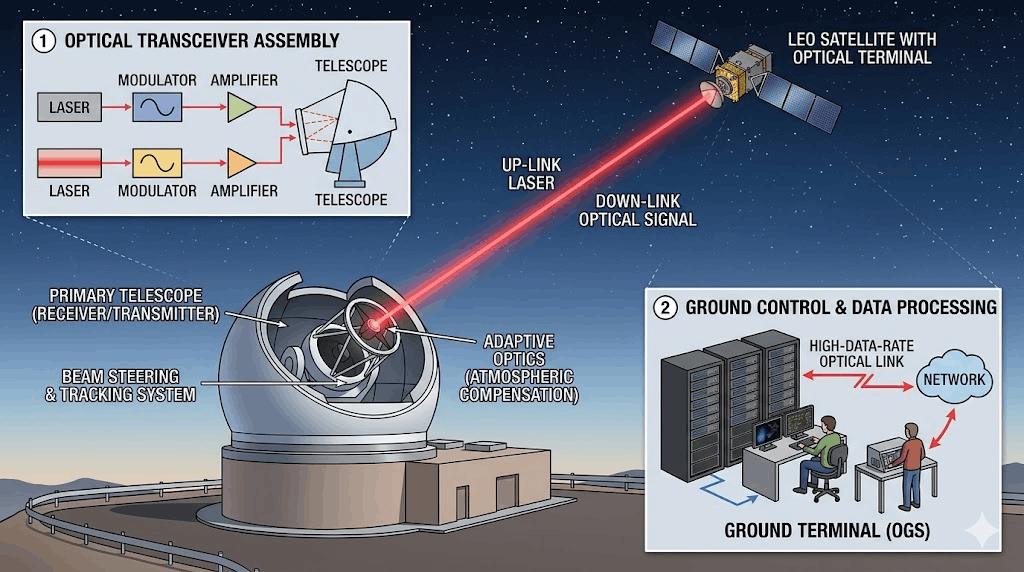

Optical ground station procurement involves decisions that sit at the intersection of precision optics engineering, space operations requirements, atmospheric physics, and site selection geography that few other infrastructure categories combine in a single procurement context. The telescope aperture must match the satellite's transmit power and link budget over the expected communication range. The site must have sufficient clear sky days annually to achieve usable contact frequency. The adaptive optics system must compensate for the local atmospheric turbulence profile. And the tracking system must achieve angular pointing accuracy sufficient to maintain the optical link across the satellite's pass arc. Getting these decisions right requires intelligence that goes substantially beyond headline market sizing. The Satellite Optical Ground Station Market Report published by The Insight Partners delivers that intelligence across four segmentation dimensions and five world regions for the confirmed 12.8% CAGR from US$ 62,013.92 million in 2023 to US$ 162,540.60 million by 2031.

The study covers the 2023 to 2031 forecast period with historic data from 2021 to 2022 and 2023 as the base year, providing country-level market sizing across all four segmentation dimensions in all five world regions.

Get exclusive insights into the Satellite Optical Ground Station Market – https://www.theinsightpartners.com/sample/TIPRE00029898

The dual-lens demand and supply methodology examines how rising debris threats, satellite population growth, and Earth observation data volume requirements translate into OGS procurement demand across each operation, equipment, application, and end-user segment in each regional market. The demand lens separately models government security and space safety program demand, commercial Earth observation and constellation operator demand, and scientific research program demand as three channels with distinct procurement timelines and geographic concentrations. The supply lens examines competitive positions, telescope and adaptive optics system development capability, laser satcom terminal technology, network design and installation capability, and government program qualification credentials across the ten profiled companies. PEST analysis contextualizes each region's national space agency investment, space debris mitigation regulatory framework, defense satellite program trajectory, and commercial satellite sector development.

Competitive Landscape

Q1. What confirmed market trajectory and CAGR does the satellite optical ground station report establish?

The market grows from US$ 62,013.92 million in 2023 to US$ 162,540.60 million by 2031 at a confirmed 12.8% CAGR as published by The Insight Partners, with country-level market sizing across all four segmentation dimensions in all five world regions.

Q2. What three demand channels does the report model within the satellite optical ground station market?

Government security and space safety program demand for SSA and debris tracking, commercial Earth observation and constellation operator demand for high-speed data downlink infrastructure, and scientific research program demand for precision satellite tracking and data acquisition are the three separately modeled demand channels.

Q3. What supply lens dimensions are most commercially significant for OGS suppliers in competitive assessment?

Telescope and adaptive optics development capability matching satellite link budget requirements, laser satcom terminal technology for free-space optical communication applications, site network design for multi-location station networks serving multiple operator customers, and government program security clearance qualification for classified SSA and defense applications are the primary supply lens dimensions.

Q4. What PEST dimensions are most significant for the satellite optical ground station market?

National space agency SSA investment and debris mitigation regulatory framework advancement, defense satellite program budgets driving classified OGS procurement, commercial satellite licensing frameworks creating the operator demand that drives commercial OGS investment, and site development regulatory environments affecting ground station location selection are the most commercially significant PEST dimensions.

Q5. Who benefits most from the satellite optical ground station market report intelligence?

OGS manufacturers and system integrators gain segment and geographic opportunity mapping for product development and market entry decisions. Satellite operators and space agencies receive technology trajectory and supplier landscape intelligence for procurement planning. Space sector investors receive validated market trajectory and competitive structure analysis for capital allocation in the space ground segment infrastructure sector.

About The Insight Partners

The Insight Partners is a one-stop industry research provider of actionable solutions. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us

The Insight Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available In: Korean | German | Japanese | French | Chinese | Italian | Spanish