Advancements in Rare Eye Disorder Therapies Propel Aniridia Treatment Market

Causes |

2026-02-25 05:58:08

Boeing's 737 MAX production is ramping toward its target monthly delivery rate. Airbus's A320 family production is expanding. Both manufacturers carry multi-year backlogs representing thousands of aircraft whose brake systems will need to be specified, manufactured, and installed before delivery, then replaced on predictable cycles throughout each aircraft's 25 to 30-year operational life. The arithmetic of this demand pipeline is straightforward: more aircraft entering service means more brake stacks installed per year on OEM production lines, and the growing in-service fleet means more brake replacement events per year through MRO cycles. Combined, these two mechanisms create a demand base for aircraft brakes that compounds with the fleet rather than growing linearly. The Aircraft Brake Market Growth at a confirmed 6.6% CAGR from 2025 to 2031, growing from US$ 9.10 billion to US$ 14.24 billion, reflects both mechanisms operating simultaneously across commercial and military aircraft end-user segments.

The study uses 2024 as the base year and draws on historic data from 2021 to 2023. Both growth drivers were building through the historic period as post-pandemic commercial aviation recovery accelerated and defense procurement expanded.

Get exclusive insights into the Aircraft Brake Market – https://www.theinsightpartners.com/sample/TIPRE00004965

Growth Driver 1: Growing Aircraft Production and Deliveries

Airbus delivered 766 aircraft in 2023 and Boeing delivered 528, with both manufacturers targeting significant production rate increases through the mid-2020s to address backlogs exceeding 14,000 combined aircraft. Each commercial aircraft delivery includes a complete brake system installation. Each military aircraft procurement adds defense-specification brake stacks at per-aircraft values that exceed commercial equivalents through more demanding performance specifications. The next-generation aircraft entering the delivery pipeline, including the Airbus A321XLR and Boeing 737 MAX 10, create new brake specification programs that generate development contract revenue before production brake deliveries begin. Production rate increases at both OEMs create directly proportional increases in brake installation demand on their respective production programs.

Growth Driver 2: Growth of the MRO Industry

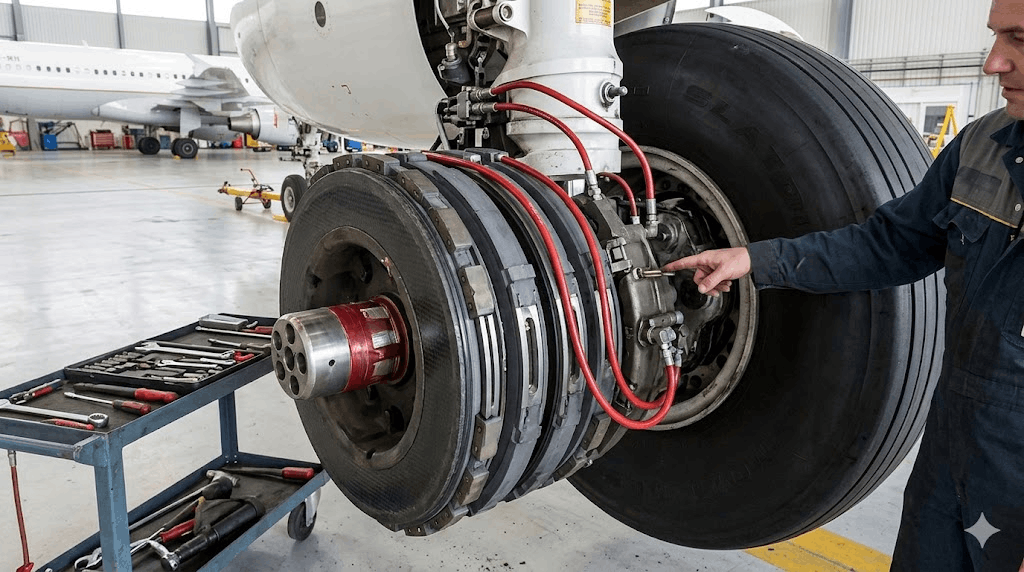

Carbon brake disc replacement is a high-frequency MRO event because carbon brake discs wear with each landing cycle, creating service life limits measured in landing cycles rather than calendar time. A busy narrowbody aircraft operating 5 to 6 flights per day accumulates brake wear cycles rapidly, requiring brake stack replacement at intervals that vary by operation intensity but typically generate brake replacement events every 1,000 to 3,000 landings depending on the specific brake specification. The global commercial MRO market is growing with the in-service fleet, with additional growth coming from the increasing concentration of MRO activity in Asia-Pacific as that region's fleet grows fastest. Each new aircraft entering service adds to the total fleet population generating MRO brake demand for the following decades.

Competitive Landscape

Q1. How do combined Airbus and Boeing production backlogs create secured near-term brake demand?

Multi-year production backlogs representing thousands of contracted deliveries translate directly into secured OEM line-fit brake procurement for manufacturers qualified on each production program, providing demand visibility that allows brake manufacturers to plan production capacity expansion with confidence about the minimum order volumes the OEM programs will require through the forecast period.

Q2. What determines the frequency of carbon brake disc replacement in commercial aircraft operations?

Carbon brake disc service life is measured in landing cycles rather than calendar time, with operational intensity determining replacement frequency. High-frequency short-haul operations accumulating six or more landings per day reach service limits significantly faster than long-haul operations with fewer daily cycles, creating replacement event rates that vary by airline operation type and are higher in aggregate per aircraft for short-haul operators than long-haul equivalents.

Q3. Why does the growing in-service fleet generate MRO brake demand that compounds rather than growing linearly?

Each aircraft delivered adds to the total population requiring periodic brake replacement for the duration of its operational life, meaning the annual MRO brake replacement pool grows not just from new aircraft entering service but from all aircraft added in previous years continuing to generate replacement events, creating a compounding base of annual demand that grows larger than new delivery rates alone would suggest.

Q4. How do next-generation aircraft programs create brake revenue above production replacement demand?

New aircraft model development programs require brake system design qualification testing before production deliveries begin, generating development contracts and prototype qualification testing revenue in the years preceding production that add to the market revenue flowing from existing program production, creating a development phase revenue layer on top of production program demand.

Q5. Why do both MRO and OEM demand streams sustain 6.6% CAGR simultaneously rather than one substituting for the other?

OEM demand grows with production rate increases at Airbus and Boeing. MRO demand grows with the total in-service fleet population, which increases with every new delivery regardless of whether that delivery was driven by fleet expansion or aircraft retirement replacement. The two demand streams operate from completely different budget pools, procurement organizations, and timing cycles, making them independently growing channels that compound rather than offset each other.

About The Insight Partners

The Insight Partners is a one-stop industry research provider of actionable solutions. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us

The Insight Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com