Perovskite Solar Cell Market Emerges as a High-Efficiency Solution for Next-Generation Solar Energy

Causes |

2026-01-19 08:46:39

The modern defense ecosystem is increasingly defined by the speed of information and the precision of engagement. At the heart of this shift lies the Target Acquisition Systems Market Share, which represents a critical intersection of advanced sensor technology, data fusion, and autonomous decision-making. As military forces transition toward network-centric warfare, the ability to detect and track threats across multi-domain environments has become the ultimate strategic advantage. This evolution is not merely about better hardware; it is about the seamless integration of intelligence into the hands of the tactical operator.

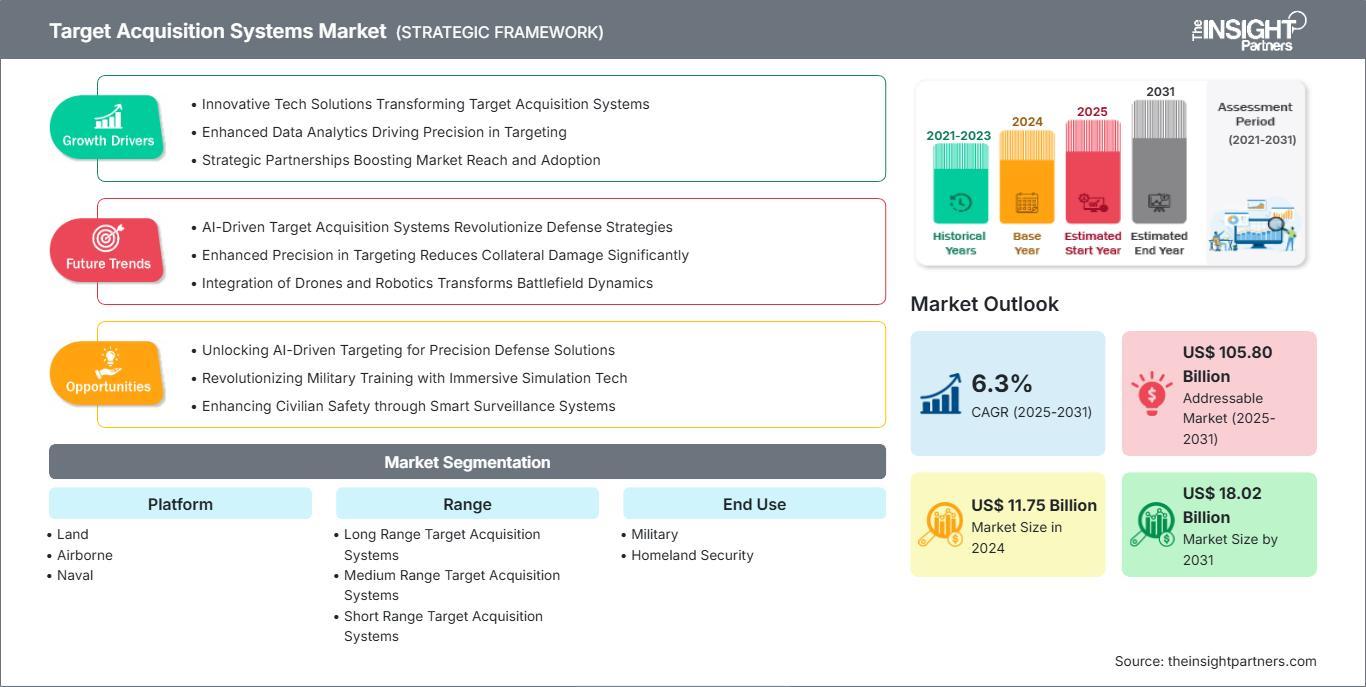

The financial trajectory of this sector underscores its growing importance in national security agendas. The Target Acquisition Systems Market size is expected to reach US$ 18.02 billion by 2031. Furthermore, the market is anticipated to register a CAGR of 6.3% during 2025 to 2031. This growth is underpinned by a global push for modernization, as aging analog systems are replaced by digital-first architectures capable of identifying targets with near-instantaneous accuracy

Download Sample Report - https://www.theinsightpartners.com/sample/TIPRE00006609

Primary Market Drivers: Catalyzing Technological Integration

The expansion of the target acquisition landscape is propelled by several key drivers that reflect the changing nature of 21st-century conflict.

1. Dominance of Multi-Sensor Fusion

The battlefield is no longer a place of single-source intelligence. Today’s market is driven by the demand for "sensor fusion," where data from Electro-Optical/Infrared (EO/IR) sensors, radar, and laser rangefinders are combined into a single, unified picture. This reduces the time between detection and engagement (the "sensor-to-shooter" link), allowing commanders to act faster than their adversaries. The integration of high-resolution thermal imaging with AI-driven software ensures that targets can be identified even in "degraded visual environments" such as heavy smoke or extreme weather.

2. Proliferation of Unmanned and Autonomous Platforms

The rise of Unmanned Aerial Vehicles (UAVs) and Unmanned Ground Vehicles (UGVs) has fundamentally altered the dynamics. These platforms require compact, lightweight, yet highly sophisticated acquisition suites. As the defense industry shifts toward "loitering munitions" and autonomous scout drones, the need for miniaturized sensors that do not compromise on range or clarity has become a top priority. This driver is particularly strong in the airborne segment, which is seeing rapid growth due to the cost-effectiveness of drone operations.

3. Shift Toward Network-Centric Warfare

Modern military strategy relies on the ability of different units—whether on land, at sea, or in the air—to share targeting data in real time. Systems are no longer isolated components on a single vehicle; they are nodes in a larger digital network. This shift drives the market for interoperable software and secure communication links, ensuring that a target acquired by a high-altitude drone can be instantly engaged by a ground-based artillery battery miles away.

4. Urgent Need for Counter-UAS (C-UAS) Solutions

The increasing use of small, inexpensive drones by both state and non-state actors has created an urgent driver for specialized target acquisition systems. Forces now require high-speed tracking systems capable of detecting "low, slow, and small" targets that traditional radar might miss. This has led to increased investment in acoustic sensors and specialized EO/IR tracking systems designed specifically for short-range air defense.

Top Players and Competitive Analysis

The competitive landscape is a blend of traditional defense "Primes" and specialized technology innovators. These companies are aggressively pursuing R&D to maintain their through proprietary AI algorithms and enhanced sensor sensitivity.

|

Key Player |

Core Focus Area |

|

Lockheed Martin Corporation |

Integrated fire-control and advanced airborne targeting pods. |

|

RTX (Raytheon Technologies) |

Multi-spectral targeting systems and high-end radar integration. |

|

Elbit Systems Ltd. |

Helmet-mounted displays and autonomous ground-based acquisition. |

|

Thales Group |

Naval optronics and soldier-portable laser designators. |

|

BAE Systems |

Precision guidance and electronic-warfare integrated sensors. |

|

Leonardo S.p.A. |

High-performance infrared sensors and airborne surveillance. |

|

Hensoldt |

Specialized radar and optronics for border security and land platforms. |

|

Rheinmetall AG |

Digital sensor suites for next-generation armored combat vehicles. |

Regional Highlights and Future Outlook

While North America remains a dominant force due to its early adoption of AI-integrated combat systems, the Asia-Pacific region is emerging as a high-growth hub. Strategic border tensions and a push for domestic defense manufacturing in nations like India and South Korea are driving significant procurement of localized target acquisition technology.

In Europe, the focus has shifted toward high-intensity conflict readiness. This has sparked a renewed interest in land-based acquisition systems for main battle tanks and infantry fighting vehicles. As the market moves toward 2031, the defining trend will be "cognitive sensing"—systems that use deep learning to filter out background noise and prioritize the most lethal threats automatically.

The transition from US$ 13.27 billion in 2025 to a projected US$ 18.02 billion by 2031 reflects more than just financial growth; it represents a fundamental change in how security is maintained. With a CAGR of 6.3%, the industry is set to remain a cornerstone of the broader defense electronics sector for the foreseeable future.

Email: sales@theinsightpartners.com

Phone: +1-646-491-9876

Also Available in :